iDeCo features

iDeCo: An additional pension you can join and choose on your own

○ The individual-type defined contribution pension plan (iDeCo) is a private pension plan based on the Defined Contribution Pension Act. Enrolling in the plan is optional.

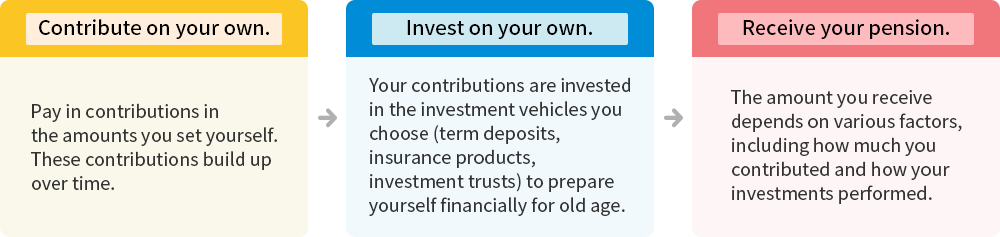

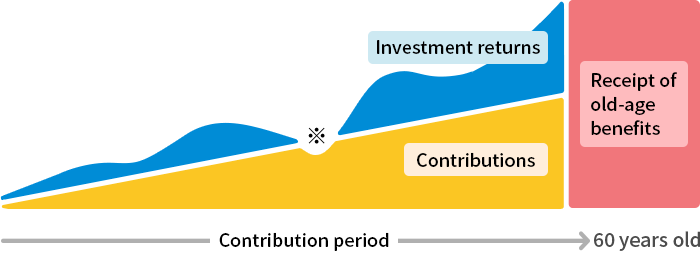

○ With iDeCo, you apply, make contributions, and select the investment approach. Your benefits reflect the total of your contributions and investment returns.

○ Special tax breaks also apply to contributions, investment returns, and when receiving benefits.

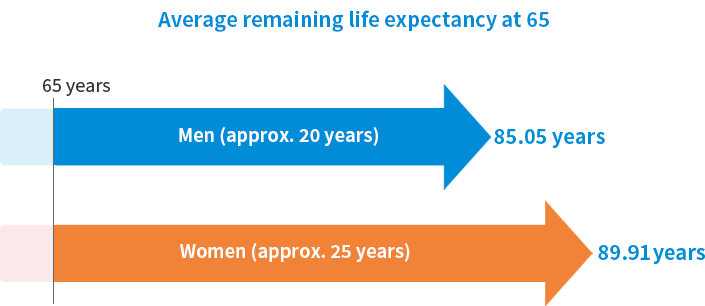

○ Japan is said to have one of the world’s longest average life expectancies. Individuals who are currently 65 have an average remaining life expectancy of 20.05 years for men and 24.91 years for women (2020 Abridged Life Table, Ministry of Health, Labour and Welfare). This means many people have more than two decades of life to look forward to after turning 65.

○ As we move toward an era in which people may routinely live to an age of 100, it’s increasingly important to prepare for a lengthy retirement. It’s a good idea to start by checking your public pension status and considering how much money you’ll have. You’ll need to take into account things like lump-sum retirement bonuses and corporate pensions.

○ After doing that, you might want to consider enrolling in the iDeCo plan as a way to gather the assets you’ll need to enjoy a more comfortable retirement while gaining access to tax breaks.

Overview of iDeCo

○ iDeCo is a pension plan that lets you decide how to invest the contributions you make to build your assets. You can make contributions into the plan until the age of 65* and begin receiving old-age benefits at 60.※

- *Certain conditions apply.

- ※In principle, assets cannot be withdrawn until you turn 60.

Once you begin receiving iDeCo old-age benefits, you will no longer be able to make contributions.

○ In general, anyone from the age of 20 until becoming 65※ can enroll in the plan. The plan is positioned and designed as an asset accumulation method to allow as many people as possible to enjoy a more comfortable retirement.

- ※Certain conditions apply.

- ※Some investment vehicles guarantee the principal. However, if you choose to invest in investment trusts or other vehicles, the value of your plan may fall below the amount of the principal.

- *1The age at which you begin receiving benefits will depend on various factors, including how long you’ve been enrolled.

Advantages of iDeCo

Three tax breaks with iDeCo

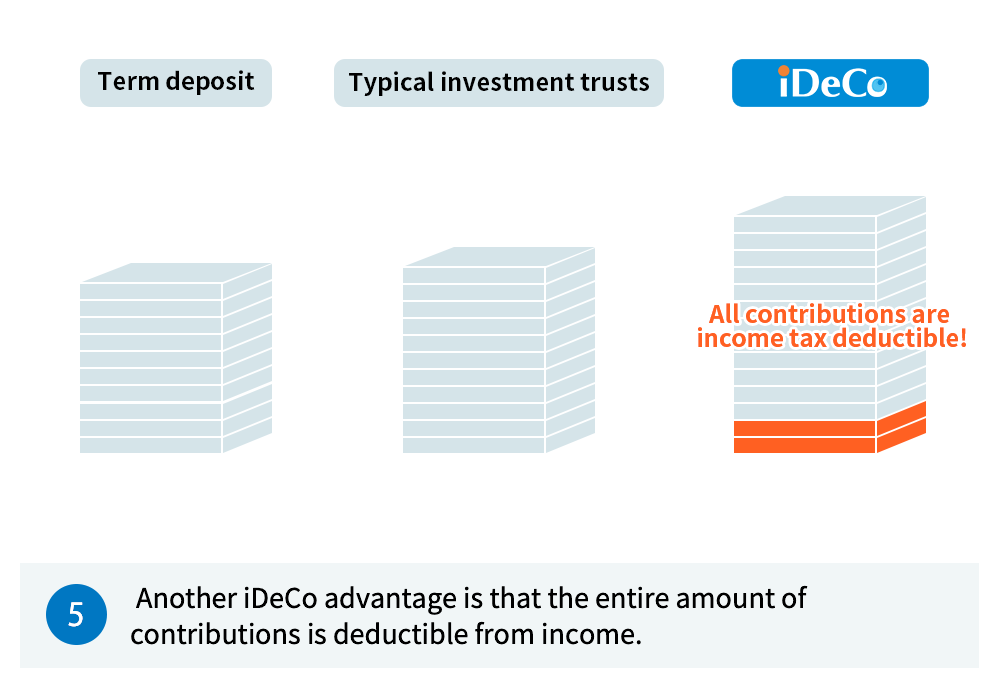

1. All contributions are income tax deductible!

○ The full amount of contributions is eligible for income tax deductions (small-scale corporate mutual aid association contribution deduction). For example, if you pay 10,000 yen every month and you pay 10% income tax and 10% resident tax, this will reduce your tax bill by 24,000 yen per year.

○ Procedures for calculating your income tax deduction differ depending on how you pay your contributions and your participant category. Try to learn as much as you can about your situation.

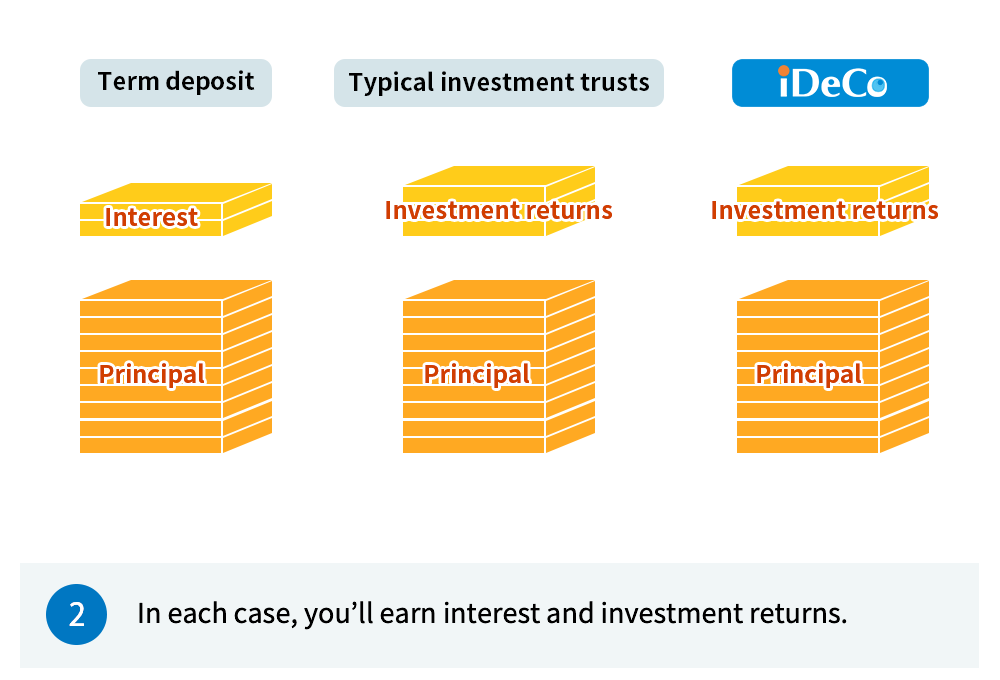

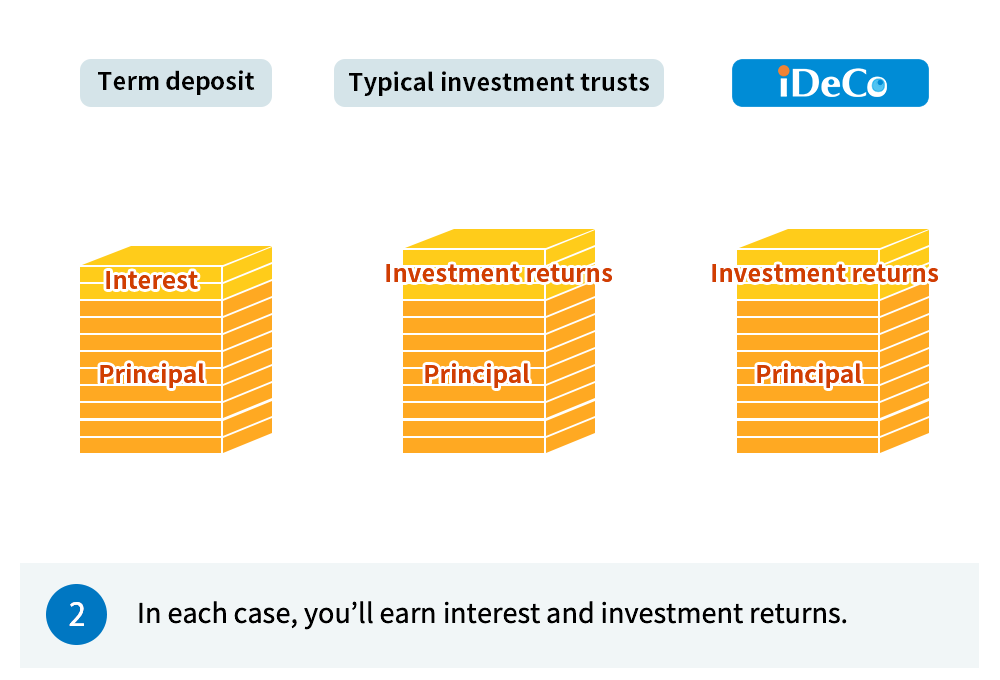

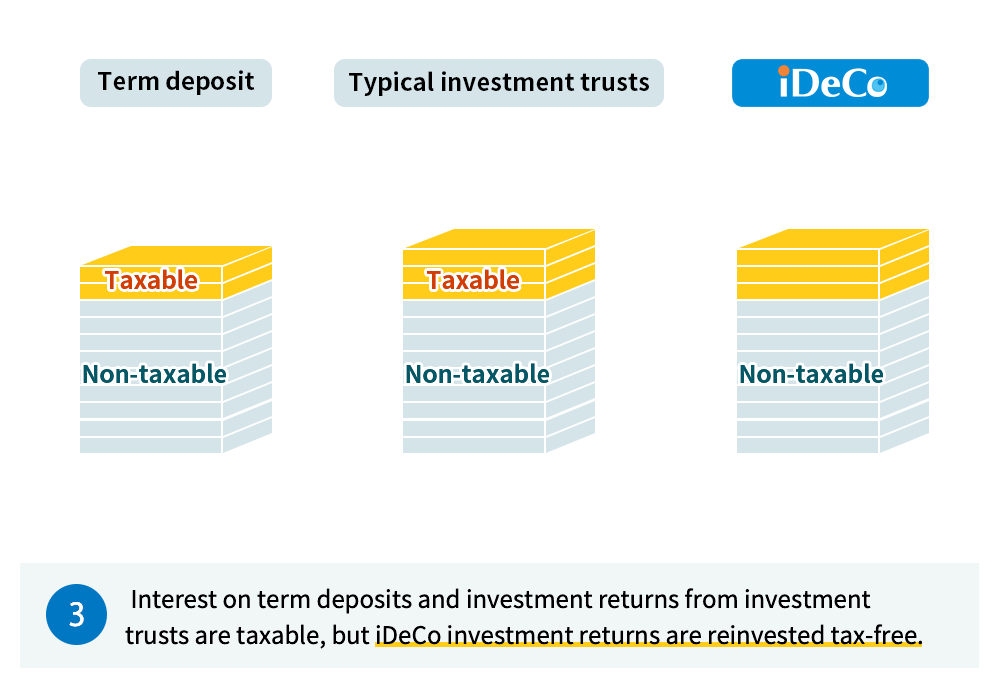

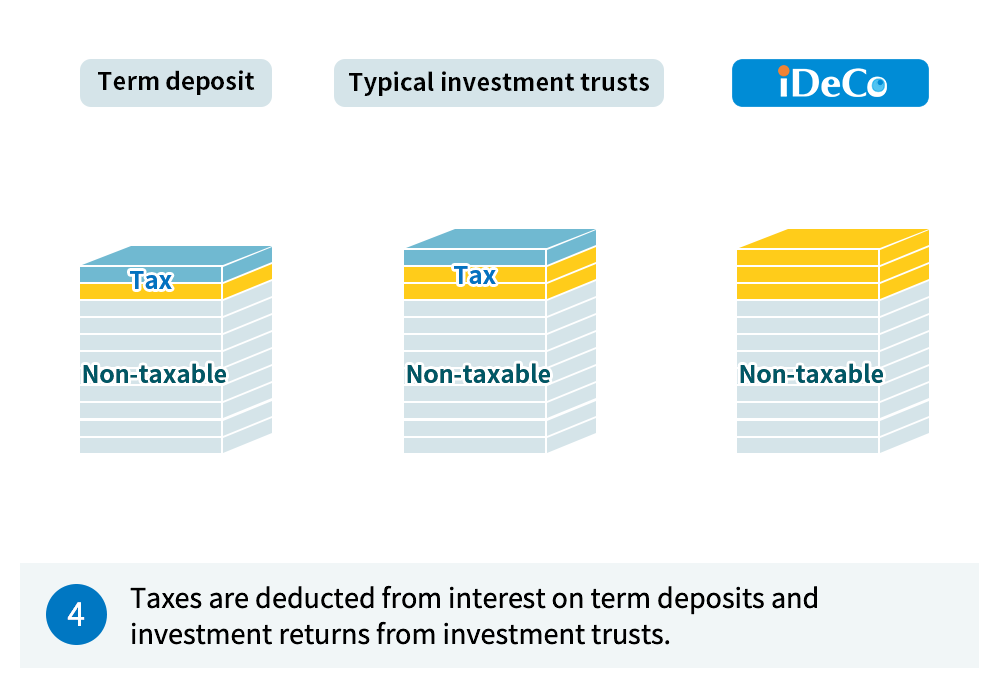

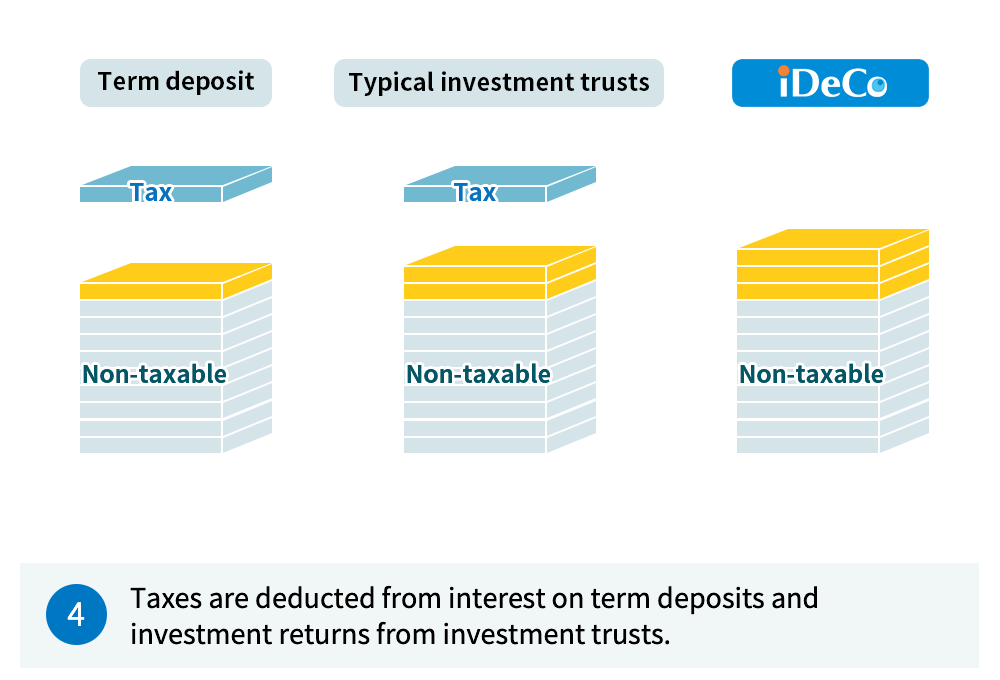

2. Investment returns are reinvested tax-free!

○ Normally, when you invest in financial products, the returns on your investments are taxed (withholding tax rate: 20.315%). With iDeCo, they’re reinvested tax-free.

- ※ The special corporation tax (1.173% per year on cumulative contributions) is currently suspended.

3. Big tax deductions also apply when receiving benefits!

○ With iDeCo, you can choose to receive either a lump sum or an annuity. (At certain financial institutions you can also choose to receive a combination of both lump sum and annuity.)

○ If you take your benefits in the form of an annuity, you are eligible for a public pension deduction; if you opt for a lump sum, you can take advantage of a retirement income deduction.

- ※ For more information on the various tax systems, refer to the website of the National Tax Agency.

iDeCo gives you peace of mind when you change jobs or retire!

○ For example, you can remain enrolled in iDeCo and continue to make contributions and invest your assets even if you get married and go from being a company employee to a full-time homemaker or if you become self-employed.

○ And you can transfer your iDeCo pension assets to another pension plan if you change jobs (portability).

Click here for more information.

How iDeCo works

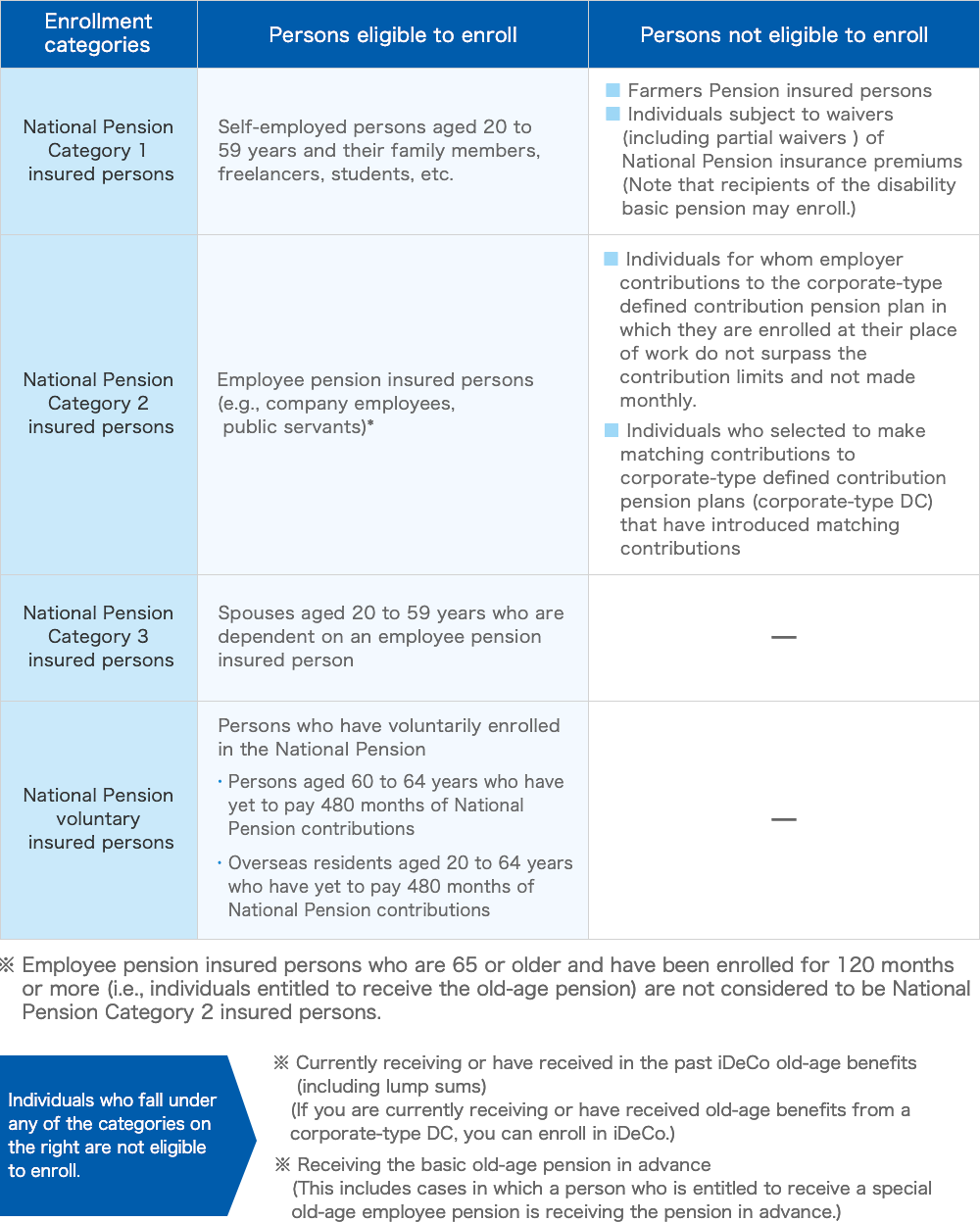

Eligibility for iDeCo enrollment and contributions

Eligibility for iDeCo enrollment

○ iDeCo is available to those who meet the following criteria:

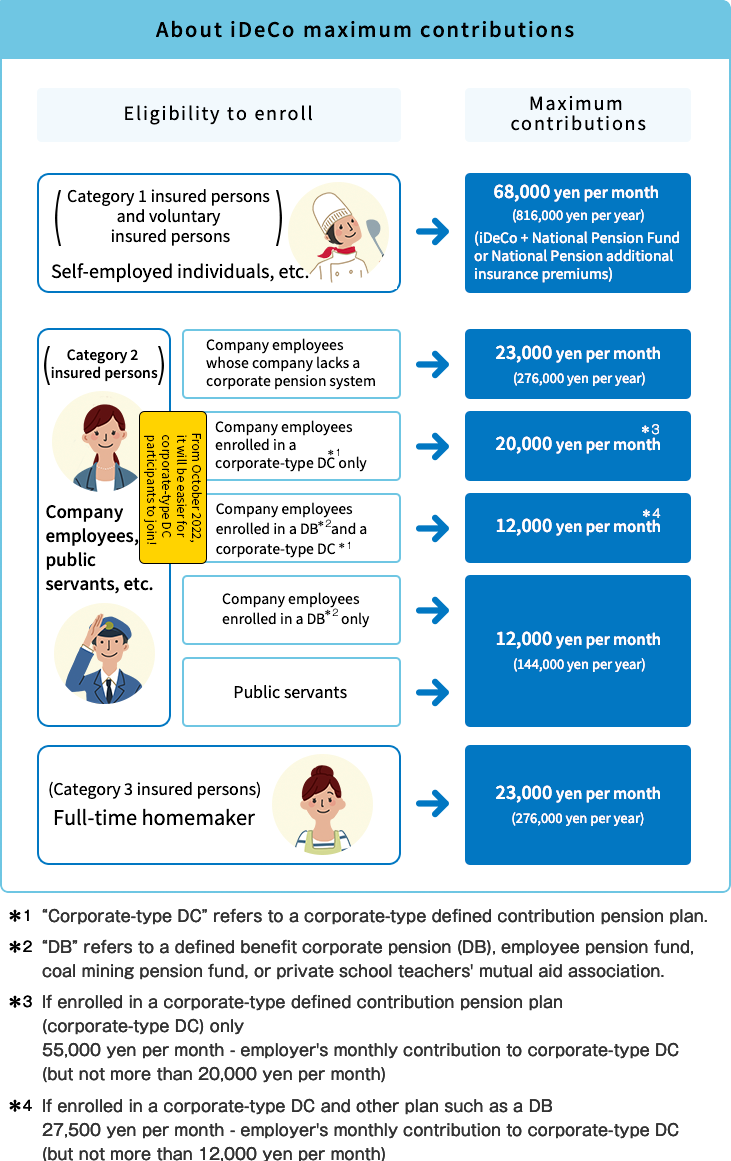

iDeCo contributions are capped (maximum contributions).

○ The maximum contributions depend on The enrollment category, therefore you will need to confirm which enrollment category applies to you.

You decide how much to pay in each month. You can start even with a small amount!

○ You can get started with iDeCo with as little as 5,000 yen per month. Set the monthly contribution you’re comfortable with in increments of 1,000 yen.

○ Even if you don’t have a lot of money to spare, you can prepare for old age in an affordable way that suits your lifestyle.

○ Contributions are considered in annual units. A participant can make lump-sum contributions one or more times a year in the month(s) they choose (annual unit contributions).

- ※1 You are permitted to change your contribution amount once per year (between the December contribution and the November contribution of the following year).

- ※2 You can stop making contributions at any time.

- ※3 Individuals who are enrolled in a corporate-type defined contribution pension plan cannot choose annual unit contributions for their iDeCo contributions. (They can only choose fixed monthly contributions.)

About investing through iDeCo

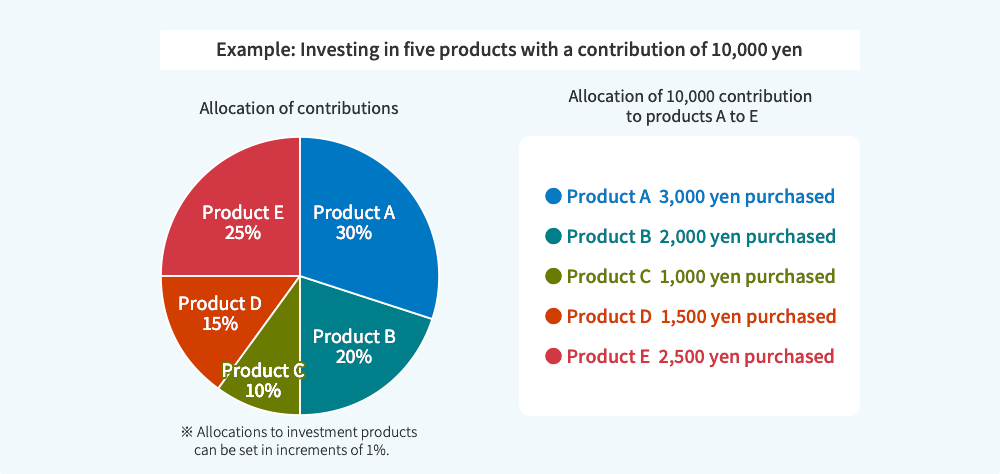

○ Choose a combination of the investment products offered by your operational management institution to invest in.

○ Select the investment products after determining your investment policy (after considering acceptable level of risk, desired rate of return, and other factors).

○ Periodically check to see how your investments are doing and make any changes in the investment products that you see fit.

You select the investment products yourself!

○ Your operational management institution can explain the investment products it offers but cannot recommend a specific product or products.

○ You need to choose products that match your investment policy and decide what to allocate to each product (i.e., what percentage of your contributions goes to which product).

○ Investment products will be purchased based on the allocation weights you determine.

- ※1 Basically, when you enroll in iDeCo, you need to decide which products you want to invest in from the investment products offered by the operational management institution (from 3–35 products; the number may exceed 35 products until the end of April 2023).

- ※2 If you enroll in the iDeCo of an operational management institution that offers a designated investment portfolio (i.e., products to be purchased if the participant does not select investment products) and you do not select investment products before a certain period elapses (a specified period of three months or more from the date of the first contribution payment after enrollment, plus a grace period of two weeks or more, as determined by the operational management institution), you will be deemed to have selected the designated investment portfolio as your investment products, and the designated investment portfolio will be purchased.

- ※3 Click here for operational management institutions offering designated investment portfolios.

- ※ Excludes fees.

How to receive iDeCo benefits

○ In general, you can receive iDeCo pension assets in the form of old-age benefits from the age of 60. You can choose when to receive your benefits at any point until you turn 75.

You can choose how to receive your benefits!

- (1) All at once in a lump sum

- ○ When you reach the age at which you are eligible to receive benefits (typically 60 years old), you can choose to receive all your benefits in a single lump sum at any point until you turn 75.

- (2) Receive as annuity

- ○ If you choose to receive iDeCo benefits as an annuity, the benefits will be treated as a fixed-term annuity (of between 5 years and 20 years).

- ○ You can choose when to start receiving benefits until you are 75 years old.

- ○ When you reach the age at which you are eligible to receive benefits (typically 60 years old), you can choose to receive your benefits over a period of between 5 and 20 years by the method determined by the operational management institution.

- ※Depending on the financial institution, you may be able to receive them as a life annuity.

- (3) Combination of lump sum and annuity

- ○ With certain operational management institutions, when you reach the age at which you’re eligible to receive benefits (typically 60 years old), you can opt to receive some of your pension assets immediately as a lump sum and the remainder in the form of an annuity.

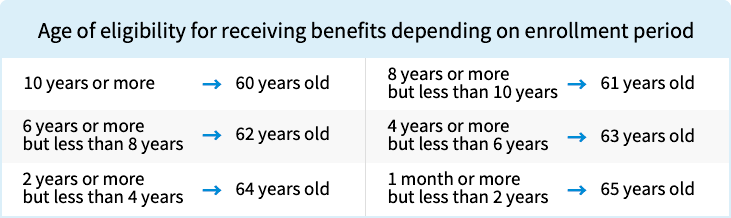

Age of eligibility to receive benefits

○ To receive pension assets from the age of 60, you must have been enrolled in iDeCo for at least 10 years (this is referred to as the total enrollment period) by the time you reach 60. If your total enrollment period is less than 10 years, the age at which you are eligible to receive benefits will be moved back accordingly.

- ※ Individuals who enroll in iDeCo for the first time at 60 or older are eligible to receive benefits from the date on which five years have elapsed since they enrolled, even without a total enrollment period.

- ※ Participants who suffer from a disability due to an injury or disease occurring or emerging before reaching the age of 75 years are eligible to receive disability benefits after a certain sustained period (one year and six months) with the disability.

- ※ You must claim your benefits before the age of 75. (If no claim is made, the benefits will be deposited at the Regional Legal Affairs Bureau.)

- ※ If a participant dies, a lump-sum payment for death will be provided to his or her surviving family.

Procedures for claiming lump-sum withdrawal payments

As a general rule, you cannot cancel your individual defined contribution pension plan (iDeCo) for a refund. However, if you meet all of the payment requirements in 1 through 7 below, you will be eligible to receive a lump-sum withdrawal payment:

- <Payment requirements>

-

- Under 60 years of age

- Not enrolled in a corporate-type defined contribution pension plan

- Ineligible to join an individual defined contribution pension plan (iDeCo) (e.g., individuals exempt from paying national pension premiums or foreign nationals residing overseas)

- Not an overseas resident with Japanese nationality (aged 20 to 59 years)

- Not a recipient of disability benefits under a defined contribution pension plan

- A total contribution period of five years or less or amount of assets under individual management of 250,000 yen or less

- Within two years from the date of the last disqualification from a corporate-type defined contribution pension plan or individual defined contribution pension plan (iDeCo)

- <Where to claim benefits>

-

If you wish to claim the lump-sum withdrawal payment, where you can submit the claim depends on your specific situation.

- (For investment directors of individual defined contribution pension plans)

-

- Please submit a “Lump-Sum Withdrawal Payment Ruling Request Form” to the records-related operational management institution for your individual defined contribution pension plan. The records-related operational management institution will handle procedures for disbursement of lump-sum withdrawal payments.

- The format of the Lump-Sum Withdrawal Payment Ruling Request Form and the documents that need to be attached are prescribed by the records-related operational management institution. Please consult the records-related operational management institution for more information on the procedure.

- (For individuals who have been disqualified from a corporate-type defined contribution pension plan and have individually managed assets in both a corporate-type defined contribution pension plan and an individual defined contribution pension plan (iDeCo) and individuals who have been automatically transferred to the National Pension Fund Association (specified operational management institution))

-

- Please submit a Lump-Sum Withdrawal Payment Ruling Request Form / Individually Managed Asset Transfer Request Form to the selected operational management institution. The specified operational management institution will handle the procedure for disbursement of lump-sum withdrawal payments.

- Please consult the operational management institution for information on how to obtain a Lump-Sum Withdrawal Payment Ruling Request Form / Individually Managed Asset Transfer Request Form, which documents need to be attached, and so forth.

- (For individuals who have been disqualified from a corporate-type defined contribution company pension plan [individuals who have not been automatically transferred])

-

- If you meet the requirements for receiving a Lump-Sum Withdrawal Payment from an individual defined contribution pension plan, you can complete the procedures with the operational management institution you were enrolled with at your place of work. For more information, please contact the operational management institution for your place of work.

Procedures for claiming Lump-Sum Death Benefits

In the event of the death of an individual-type defined contribution pension plan (iDeCo) participant, investment director, or automatic transferee (individual whose individually managed assets have been transferred to the National Pension Fund Association (specified operational management institution) without completing the procedures within six months after being disqualified from a corporate-type defined contribution pension plan), the surviving family can receive a Lump-Sum Death Benefit. However, note that the assets will be treated as inherited property after five years from the date of death.

If no claim is submitted after the assets are treated as inherited property, they will be deposited with the Regional Legal Affairs Bureau.

- <Where to claim benefits>

-

If you wish to claim a Lump-Sum Death Benefit, where to submit the claim depends on the situation of the deceased.

- (For former individual defined contribution pension plan participants / investment directors)

-

- The surviving family should submit a “Participant Death Notification Form” to the operational management institution for the individual defined contribution pension plan that the deceased had chosen.

Please consult the operational management institution for information on how to obtain the Participant Death Notification Form, the administrative procedures involved, and so forth. - Please attach a death certificate or documents attesting to the death to the Participant Death Notification Form. (Copies of such attached documents are also valid.)

- In addition to submitting the Participant Death Notification Form to the abovementioned operational management institution, submit a Lump-Sum Death Benefits Ruling Request Form to the records-related operational management institution managing the deceased’s individually managed assets. The records-related operational management institution will handle the procedures for the payment of Lump-Sum Death Benefits.

The format of the Lump-Sum Death Benefit Ruling Request Form and the documents that need to be attached are specified by the records-related operational management institution. Consult the records-related operational management institution for information on these procedures.

- The surviving family should submit a “Participant Death Notification Form” to the operational management institution for the individual defined contribution pension plan that the deceased had chosen.

- (For individuals who were automatic transferees)

-

- The surviving family must submit a Lump-Sum Death Benefit Ruling Request Form to the operational management institution. The specified operational management institution will handle the procedure for payments of Lump-Sum Death Benefits.

- Please consult the operational management institution for information on how to obtain a Lump-Sum Death Benefit Ruling Request Form, what documents need to be attached, and so forth.

Portability between pension plans

○ iDeCo pension assets are portable. Completing the specified transfer procedures allows you to take your pension assets with you when you change jobs or leave a job.

○ Additionally, as long as certain criteria are met, you can carry over assets from other pension systems (e.g., defined benefit corporate pensions, corporate-type defined contribution pensions).

○ For more information on the transfer procedures, please consult your operational management institution.

Important points

In principle, benefits cannot be received until you turn 60.

○ Since iDeCo is a pension plan designed to accumulate assets for old age, it is subject to tax breaks.

○ This means you will generally not be permitted to withdraw pension assets (contributions made and investment returns earned) until you turn 60.

○ Note that your total enrollment period will determine the age at which you can receive your benefits.

○ Individuals who enroll in iDeCo for the first time at 60 years of age or older are eligible to receive benefits from the date on which five years have elapsed since they enrolled, even without a total enrollment period.

○ However, if an iDeCo participant suffers more than a certain level of disability or a participant dies, disability benefits or a Lump-Sum Death Benefit can be received even if age 60 was not reached when this occurred.

The amount of benefits participants receive will vary depending on the performance of their investments.

○ With defined contribution pension plans, the amount of money to be received in the future isn’t fixed.

○ Participants are personally responsible for the investment of their assets. The benefits they receive will vary depending on the performance of their investments.

○ Investment products include products that do not guarantee the principal, therefore please select products based on a thorough understanding of their characteristics.

Additionally, please note the following:

○ Fees apply. (The amount of these fees will depend on the financial institution.)

○ Individuals with no taxable income will not benefit from income tax deductions for contributions.

○ The income tax deduction applies only to the participant’s income. Spouses are not eligible to receive income tax deductions.

○ Investment assets are also subject to the separate special corporation tax; however, this tax is currently suspended.